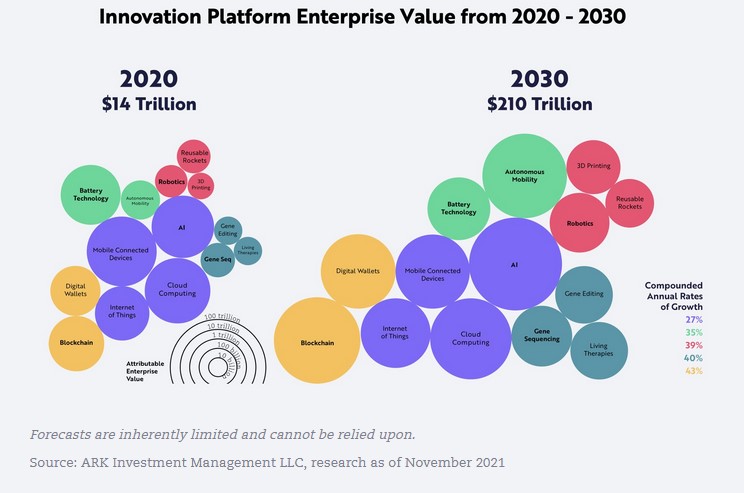

The Growth of Innovation

The Forecast highlights the possible growth in technologies into 2030.

Our Firms has uncovered investment vehicles to give investors the opportunity to grow their net worth. Innovation is under owned in portfolios through the major indexes in the U.S. Adding innovative companies to your portfolio may increase your diversification and results.

Securities offered through Newbridge Securities Corp., Member FINRA/SIPC. Investment Advisory Services offered through Newbridge Financial Services Group, Inc., an SEC Registered Investment Adviser. Office of Supervisory Jurisdiction: 1200 North Federal Highway, Suite 400 Boca Raton, FL 33432 (954) 334-3450. Zoellner Whole Financial, Newbridge Securities Corp. or NFSG is not affiliated with Estate Planning Team, Inc. http://www.newbridgesecurities.com http://www.brokercheck.org http://www.finra.org http://www.sec.org.http://www.sipc.org. Recommendations made by members of the Estate Planning Team, including the Deferred Sales Trust or other tax, legal or estate planning strategies should not be construed to be endorsed by Newbridge Securities Corporation or Newbridge Financial Services Group, Inc.